Credit Union Strategy Execution Playbook

Credit union strategy execution depends on trust: trusted metric definitions, trusted ownership, and a pre-read leaders actually consume. Elate helps credit unions run strategy as a governed execution rhythm with owners, thresholds, updates, risks, and executive-ready reporting, without replacing BI, Planner, Teams, or core systems.

From Goal-Setting to Goal Execution: What Credit Unions Need to Make Strategy Stick

Key Takeaways:

- Strategy fails without prioritization and structure

- OKRs break when everything becomes an objective

- Execution requires a consistent operating rhythm

- Reporting should drive decisions, not just updates

What is strategy execution in a credit union?

Strategy execution in credit unions is the process of aligning strategic goals with day-to-day work, tracking progress consistently, and enabling leadership to make timely decisions based on clear, reliable data.

Why Strategy Execution Stalls in Credit Unions

For many credit unions, the problem isn’t whether Leadership believes in goals. It’s not a lack of strategic intent. It’s not a lack of planning. And it’s usually not a lack of effort.

In fact, many of the organizations that struggle with strategy execution care deeply about making it work.

And still, it stalls.

When strategy doesn’t stick, most often it’s because strategy gets harder to operationalize as the organization grows.

Long-term vision lives in one place. Department priorities live somewhere else. Progress updates happen inconsistently. Reporting gets rebuilt right before Leadership reviews or Board deadlines. Some teams are highly metric-driven. Others report more anecdotally. Everyone is trying to contribute to the same strategy, but they are not always working from the same structure.

What looks like a planning problem is often an execution problem.

The strategy exists. The challenge is creating a shared system for how that strategy gets translated, reviewed, updated, and acted on across the org.

This is where many credit unions start looking for a more structured way to manage execution, often evaluating a strategy execution platform to bring consistency, visibility, and alignment across teams.

Quick Check: Signs Your Execution Model Is Breaking Down

If several of those sound familiar, you’re probably not dealing with a motivation problem. You’re dealing with a design problem:

- You’ve tried to roll out OKRs before, but they never fully stick.

- Leadership believes in goal alignment, but teams still define progress differently.

- Updates happen in bursts right before a Board report or Leadership meeting.

- Some OKRs are outcomes, while others are projects, audits, or implementation steps.

- People can see the strategy at a high level, but not always how their work connects to it.

- Reporting feels reactive, inconsistent, or overly manual.

- The process feels heavier every quarter instead of more natural.

These aren’t isolated frustrations. They’re symptoms of the same underlying issue: an organization with strategic goals, but no shared operating model for executing them.

Common Credit Union Strategy Execution Challenges

These challenges tend to show up in a few consistent ways:

- Misalignment between leadership priorities and team execution

- Inconsistent progress updates across departments

- Too many priorities with no clear ranking

- Reporting that is reactive instead of proactive

- Difficulty connecting daily work to strategic outcomes

- Manual, time-consuming board reporting processes

These issues don’t happen in isolation. They’re typically symptoms of the same underlying gap: a lack of a consistent execution model.

The Pattern: When Everything Important Becomes an OKR

One of the most common breakdowns in strategy execution for credit unions is that everything starts getting labeled as an OKR.

A launch becomes an OKR.

An audit becomes an OKR.

A system implementation becomes an OKR.

A deliverable becomes an OKR.

A recurring operational responsibility becomes an OKR.

That creates noise, because not all work should be measured the same way.

An Objective should reflect a meaningful outcome the organization is trying to achieve. It should have a clear purpose, measurable success criteria, and a direct relationship to the broader strategy.

A Tactic is different. It’s important work, but it’s supporting work. It exists to move the Objective forward.

When those two layers get blurred together, Leaders lose the ability to answer basic questions clearly:

- What are we actually trying to accomplish?

- How are we measuring success?

- What work is supporting that outcome?

- Where are we behind vs. in progress?

That’s when strategy starts to feel more complicated than it should. Not because there’s too much work, but because the work is being categorized in a way that makes strategic execution harder to see and harder to manage.

The Hidden Cost of Treating Strategy Like a Reporting Exercise

The obvious cost is messier reporting. The less obvious cost is that Leaders lose the ability to intervene early.

When updates are inconsistent, Leaders are often looking at stale information. By the time something shows up as a problem, it’s already late. Meetings become status collection. Board materials become a scramble. And teams spend more time reconstructing progress than managing it.

There’s also a cultural cost.

When goal-setting feels unclear or overly administrative, people stop seeing it as useful. They experience it as more work added on top of the “real” work. Which makes adoption even harder the next time around.

So the issue isn’t just inefficiency. It’s erosion of trust in the process itself.

Why Typical Frameworks Don’t Fix Credit Union Execution

At this point, many organizations try to solve this issue by tightening templates, asking for more frequent updates, or introducing a new project management tool.

But those fixes usually don’t address the real breakdown.

If teams aren’t working from shared definitions, a better template won’t fix that.

If people don’t know the difference between an Objective and a supporting Tactic, more updates won’t make reporting clearer.

If the org has already had a few false starts with OKRs, dropping software into the mix without guidance won’t suddenly create adoption.

This is especially true in credit unions, where strategy touches governance, operations, member experience, technology initiatives, risk, and cross-functional execution all at once.

The problem is not that there’s no framework. The problem is that the framework hasn’t been operationalized in a way people can actually use.

The Breaking Point: When Goal-Setting Fatigue Turns Into Skepticism

If your organization has tried to launch OKRs before and it did not stick, that history matters.

If teams have seen the language change every year, or watched priorities get re-labeled without ever becoming easier to execute, they do not approach the next rollout with excitement. They approach it with skepticism.

That skepticism is not resistance for the sake of resistance. It’s usually a rational response to friction.

We see this often: Leaders are excited by the idea of becoming more goal-driven, but the actual rollout creates confusion. Teams are asked to define OKRs without a shared definition of what qualifies as an Objective. The organization introduces the structure, but not the clarity.

Then the Board report is due, the Leadership meeting is approaching, or the monthly review is on the calendar, and suddenly everyone is rushing to reconstruct what happened.

And when that becomes the norm, the symptoms are pretty clear:

- Updates become reactive instead of useful

- Leaders get incomplete context

- Board materials turn into a scramble

- Teams start associating strategic reporting with annoyance instead of creating a bias to action

- Progress conversations happen too late to change the outcome

This is usually the inflection point. Strategy doesn’t disappear, it just becomes too frustrating to trust.

The Fix: Moving From Goal-Setting to an Execution System

The organizations that make OKRs work don’t just introduce a framework. They create an operating system around it.

That includes:

- a shared structure from long-term vision down to team-level work

- clear distinctions between Objectives and Tactics

- a lighter, repeatable reporting rhythm

- visibility into both outcomes and contextual commentary

- a rollout model that matches the organization’s maturity

This is the part too many teams underestimate.

If an organization has struggled to make strategy stick in the past, the answer is not to push harder. It’s to make the process more usable.

In most cases, that starts with Leadership.

Start with the Executive team and the Leaders who own strategic Objectives. Define the hierarchy. Create consistency. Establish the reporting rhythm. Build confidence in the process. Then expand over time.

That crawl-walk-run approach tends to work far better than forcing organization-wide adoption all at once.

See how credit unions are building this execution model →

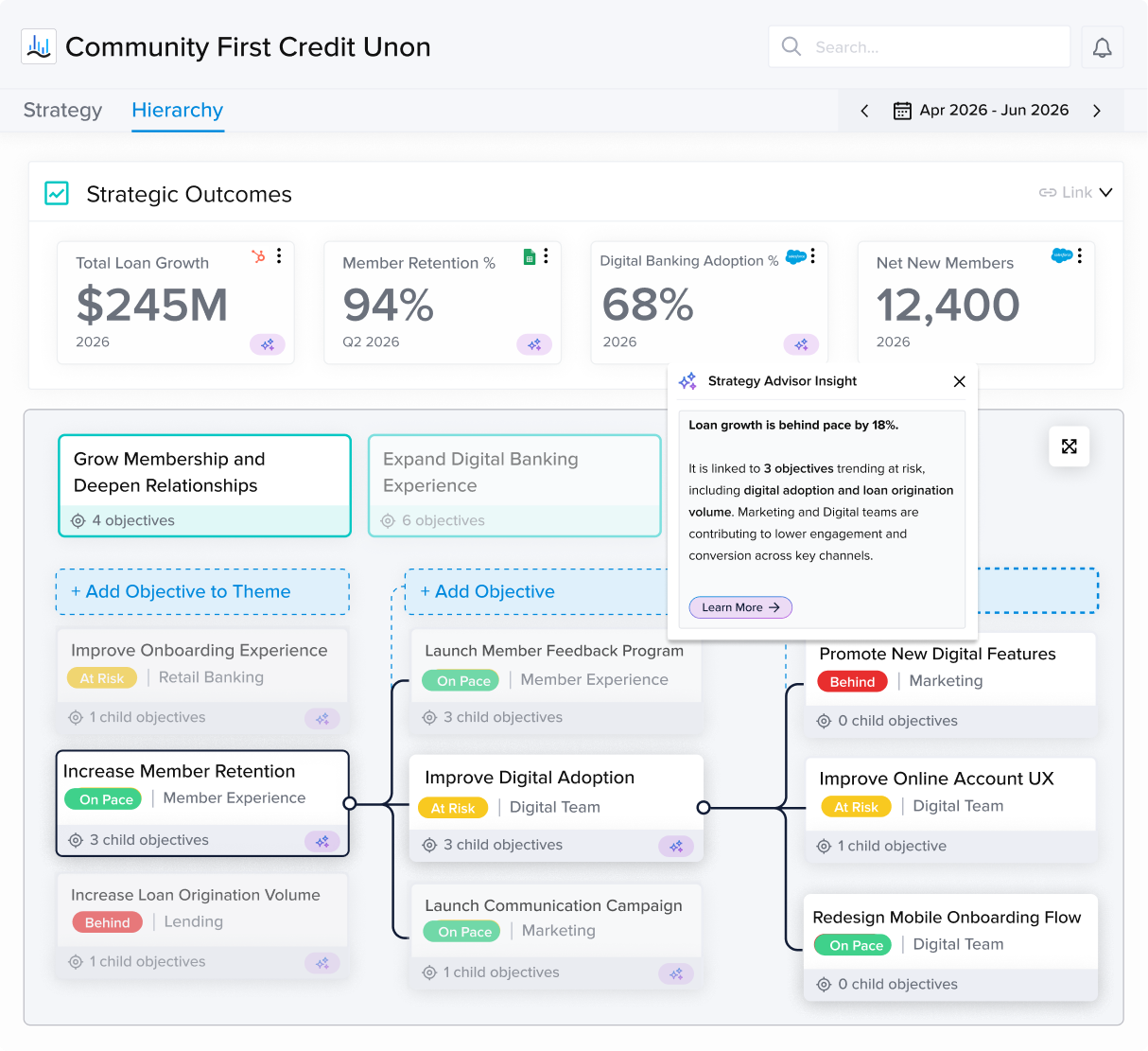

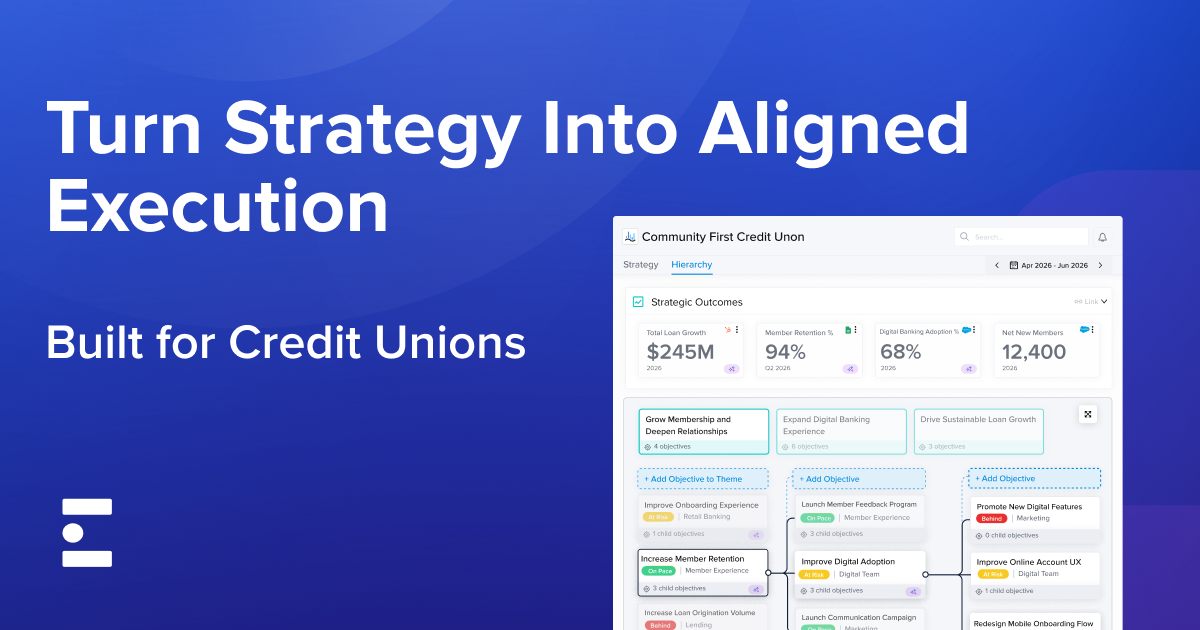

A Simple Credit Union Execution Model

Here is a structure we see work well, especially for credit unions that have strategic goals in place but need a more usable way to execute them.

1. Start with the top-level outcomes that matter most

These are the handful of operating outcomes that define whether the strategy is working. Think growth, member experience, digital adoption, efficiency, margin, or other measures the Leadership team and board consistently come back to.

These should sit above departmental work and create a common definition of success for the year.

Common trap: Listing too many operating outcomes, or choosing metrics that matter to one department but not to the organization as a whole.

Rule of thumb: If Leadership cannot quickly identify which 3-5 outcomes are most important, the strategy is probably carrying too much at the top.

2. Group work into a small number of Themes to drive prioritization

These are the major focus areas - or Themes - for the year. They are the “rallying cries” that help the organization orient around what matters most.

This is often the missing middle between a long-term vision and day-to-day departmental work.

Common trap: Making Themes too broad and generic (“Innovation,” “Excellence”) or so numerous that they stop creating any real prioritization.

What good looks like: A Leader should be able to explain how their team’s work connects to one of a small number of clearly named Themes.

3. Define Objectives as Outcomes, not activity

Each Objective should answer one question: what meaningful change are we trying to create?

This is where many credit unions get stuck. It is easier to list implementations, launches, audits, and projects than it is to define the actual outcome those things are meant to drive. But launching a new account opening process is not the same as improving funded account conversion, reducing member effort, or increasing digital adoption. So distinction matters.

Common trap: Writing Objectives that are really activities. Better: define the result you want, then place the supporting work underneath it.

A simple Objective test: If you can complete it and still not see the impact, it is probably not an Objective.

4. Use Tactics for the supporting work

This is where projects, implementations, audits, launches, and cross-functional initiatives belong.

Each Tactic should answer:

- Which Objective does this support?

- What does “done” mean?

- What does progress look like?

- What dependencies or blockers could slow this down?

Common trap: Treating the Tactics layer like a dumping ground. If something cannot be tied to an Objective, it should trigger a Leadership question: is this actually a priority, or just noise?

Why this matters: This is how credit unions stop carrying around long lists of work that all feel important but become impossible to prioritize when capacity gets tight.

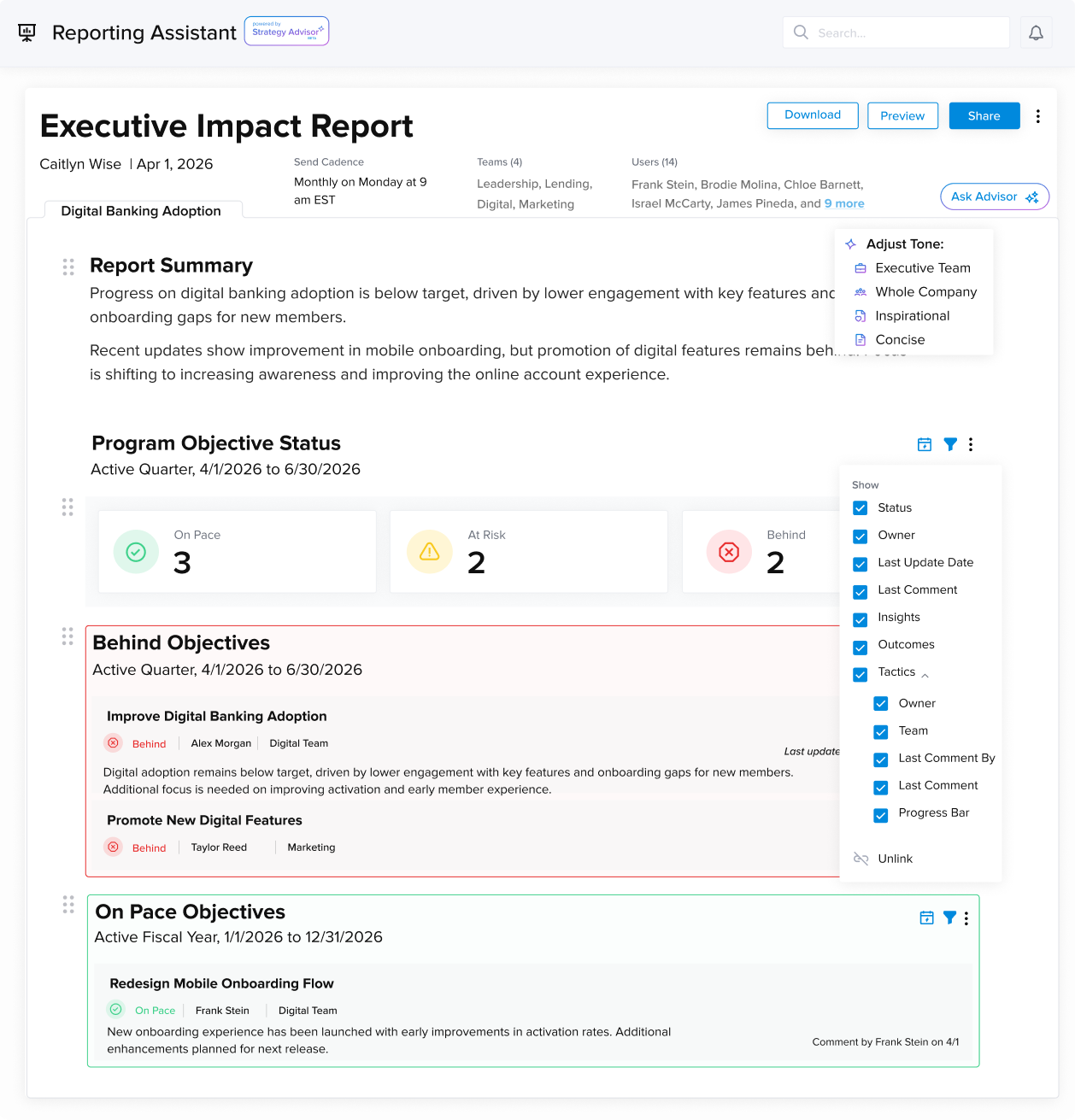

5. Create a lightweight reporting cadence

Don’t wait until the Board report is due. Build a rhythm of executive-ready reporting updates that gives Leaders earlier signals and reduces last-minute scrambling.

What we see work well:

- a regular update cadence, often monthly to start

- async progress updates before Leadership discussions

- live time reserved for decisions, tradeoffs, and support

- reporting that gives the Board and Executive team visibility without requiring a last-minute rebuild every cycle

Common trap: Using Leadership time to gather updates that could have been shared in advance. When that happens, the real conversation gets squeezed out.

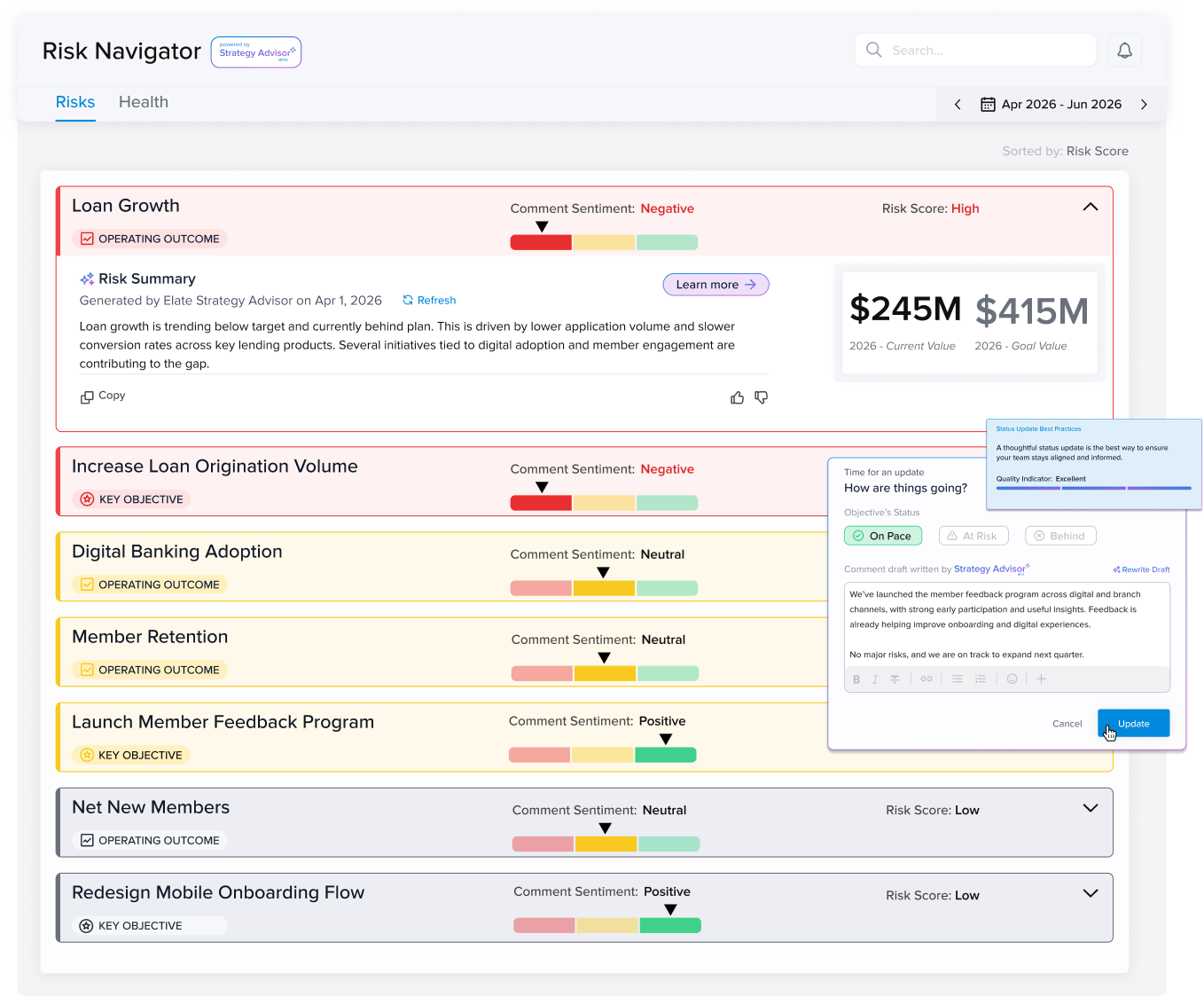

6. Bring data and narrative together

Metrics alone aren’t enough. Commentary helps explain whether the numbers reflect temporary friction, emerging risk, or meaningful momentum.

This is especially important in credit unions, where some strategic work is highly measurable and some depends on context, sequencing, or cross-functional coordination.

Common trap: Overcorrecting too far in either direction. Purely anecdotal updates create ambiguity. Purely numeric updates can hide emerging risk.

7. Roll out in phases

Start where strategic ownership is strongest. Expand once the structure and rhythm are working.

In many credit unions, the right place to start is with the Executive team and the Leaders who already own strategic Objectives. Build the structure there first. Establish the rhythm. Create visibility. Then expand over time.

Why this works: It lowers friction, builds confidence, and helps the organization learn what “good” looks like before scaling the model more broadly.

What Changes When Credit Unions Run Strategy Like a System

When credit unions move from fragmented goal-setting to a real execution system, a few things happen quickly:

- Leaders tend to spend less time chasing updates, and more time addressing risk.

- Teams understand how their work connects upward.

- Board reporting becomes more credible and less chaotic.

- Progress gets discussed earlier, when there’s still time to act

- The strategy process starts to feel like a part of the organization’s rhythm instead of a recurring fire drill

And most importantly, OKRs stop feeling like an annual rollout challenge and start becoming a usable way to run the business.

7 Elements of an Effective Strategy Execution Model for Credit Unions

To make this more concrete, here’s what a strong execution model actually includes:

- Clear top-level outcomes

- Defined strategic themes

- Outcome-based objectives

- Supporting tactics tied to objectives

- Consistent reporting cadence

- Combined data and narrative context

- Phased rollout approach

Frequently Asked Questions

What is strategy execution in a credit union?

Strategy execution is the process of turning strategic goals into measurable outcomes, aligning teams around priorities, and creating a consistent rhythm for tracking progress and making decisions.

Why do credit unions struggle with strategy execution?

Most credit unions don’t struggle with planning. They struggle with prioritization, alignment, and consistency. Strategy breaks down when updates are inconsistent, goals are unclear, and leadership lacks visibility into progress.

How are OKRs used in credit unions?

OKRs help define outcomes and measure progress, but they only work when organizations clearly separate objectives (outcomes) from tactics (work) and build a consistent execution rhythm around them.

What is the difference between an objective and a tactic?

An objective defines the outcome you want to achieve. A tactic is the work required to achieve that outcome. Confusing the two makes strategy harder to prioritize and track.

How often should credit unions review strategy progress?

Most credit unions benefit from a monthly reporting cadence with asynchronous updates before leadership meetings, allowing meetings to focus on decisions instead of status collection.

Ready to See What This Looks Like in Practice?

If your credit union is growing, modernizing, managing more cross-functional priorities, or simply feeling the strain of “too many goals and not enough visibility,” you’re not alone.

You’re at the point where informal execution stops scaling, and building a real operating system becomes part of running the strategy responsibly.

If that is the inflection point you’re in, we’d love to talk.

We can share what we’re seeing across other credit unions and walk through how Elate supports the cadence, visibility, and risk tracking described here.

Book a demo to see how Elate supports credit union strategy cadence, visibility, and risk tracking.